“Dear Mr. Money Mustache…

I’d like to retire soon. I’ve had a good career and the numbers say I’m just over the threshold, but I’m still afraid.

It would help if I had a solid plan for what to do after retirement – perhaps even make some money eventually. Because I think it would help boost my confidence to pull the plug at the old law office. But as an attorney, I’m trained to see the pitfalls of everything and frankly I’m afraid.

How do all of you fearless Mustachians just go out and start businesses and make money, when it is so hard to get started – so many details and contingencies to account for?

– the Skittish Scottsdale Solicitor

Dear SSS,

To answer a question like yours, it sometimes helps to look at a role model who has some of the traits you would like to cultivate in yourself. So this seems like the perfect time to share a story I have been wanting to tell here on MMM for at least five years. And the funny part about this tale is that it keeps getting more interesting, the longer I wait to share it.

It is the story of my long-time friend Luc, who has earned a reputation in our own community as the honey badger of entrepreneurship.

The Honey Badger

Luc takes a brief rest from digging out 30 tons of dirt from his own basement and hand-pouring a new foundation while his son supervises.

From painting houses to raising edible insects, selling handmade pine coffins to writing and shooting his own feature length film in Scotland, all while never becoming too proud to take a literal Shit Shower while cleaning the sewer lines in his own rental properties, Luc’s story never fails to amaze. And it can be especially useful for those of us on the other end of the spectrum – wannabe entrepreneurs who are still hesitating to open our first small business checking account.

This story is a great financial lesson as well. Luc’s family* has gone from zero to financial independence without the benefit of the easy tech salaries that got my own household there back in the mid 2000s. Like most of us, they have seen windfalls and setbacks over the years, but the biggest factor in getting them to a better financial place has been continuing to get the work done, while choosing not to squander all of the proceeds on an ever bigger lifestyle.

So from this interview I’m hoping you will pick up both some inspiration for continued down-to-earth hard work, and a perspective to just go out and try new things, especially in the area of entrepreneurship.

If you do it right, there is upside waiting around every corner. So let’s get into the questions!

The Man Who Never Got a Real Job

MMM: The first moment we met was in July 2005, when I had just retired and we bought our first house in old-town Longmont, with a baby on the way. Walking through my new backyard, I immediately noticed two thirtysomething dudes in dirty clothes, working up on the roof of the old garage on your side of the fence. And I thought to myself, “These are my type of people!”, and walked over to meet you.

What was going on in your life at that moment, in both life and business?

Luc: Well, considering our daughter was born nine months later, it was near the end of one phase and the beginning of the next. At the time, my primary business was a house painting company that I had started in the late ‘90s, after my biology degree wasn’t enough to get me a job at a pet store (in Boulder you need advanced degrees for that sort of thing).

I had worked pretty hard to get that painting company up and running, starting as a one-man show, then employing as many as 18 people at one point. It was a good gig in that I had a lot of free time to work on other projects in the winters, and even went back and got my Master’s degree along the way.

By 2005, though, I had severely downsized the company and I was back to a small crew. I was beginning to think about what I wanted to be when I grew up.

One project we started that year was buying and quickly fixing up a house a few blocks from our place on a street called Carolina Avenue. This was primarily achieved by leveraging the equity we had built up in our first house. I still own and rent out that place (which you subsequently helped me do a more extensive renovation on).

MMM: So then we both had these children born at almost the same time, and all six people in our two families became friends. We both started helping each other with construction projects, but when Longmont denied my building permit application to expand our tiny 600 square foot house, I decided to move out and turn that one into a rental, and move into a bigger place a few blocks away. What was the catalyst that made you leave the little leafy paradise of that street? (and yes I realize this is a leading question :-))

Luc: The first thing is that old Happy Street is a pretty busy street, and with a young daughter, we thought it might be nice to live on a quieter stretch. One day my wife and I went for a walk and picked our favorite blocks in the neighborhood. There happened to be a “beautiful” old fixer upper for sale on one of those blocks, and within a few days we were under contract.

That we were willing to take the plunge so quickly was largely because of you and your construction company. At the time, I hadn’t done any extensive remodels, but because you were willing to help me out, I figured we could make it work.

At the time, my wife was certain that it would be a fix-and-flip and there was no way she would actually live in the house. Because it started out in such bad shape, it was hard to imagine it ever becoming a nice family home, but it really did in the end. So we we moved in at the beginning of 2008 and here I sit, typing away in the office.

The Rental Real Estate Projects

MMM: So, our biggest collaborations over the years have been in fixing up houses, often rental houses that one of us owned (okay most of them were yours.) We started with The Foreclosure Project in 2011, then went back and did a major upgrade to one of your other places here in town. Most recently we did The Atwood Project, which was the inspiration for my post on Installing your own furnace.

How has your experience been in owning single family rental houses, while doing your own management and maintenance? Is it a reasonable return on your investment and labor?

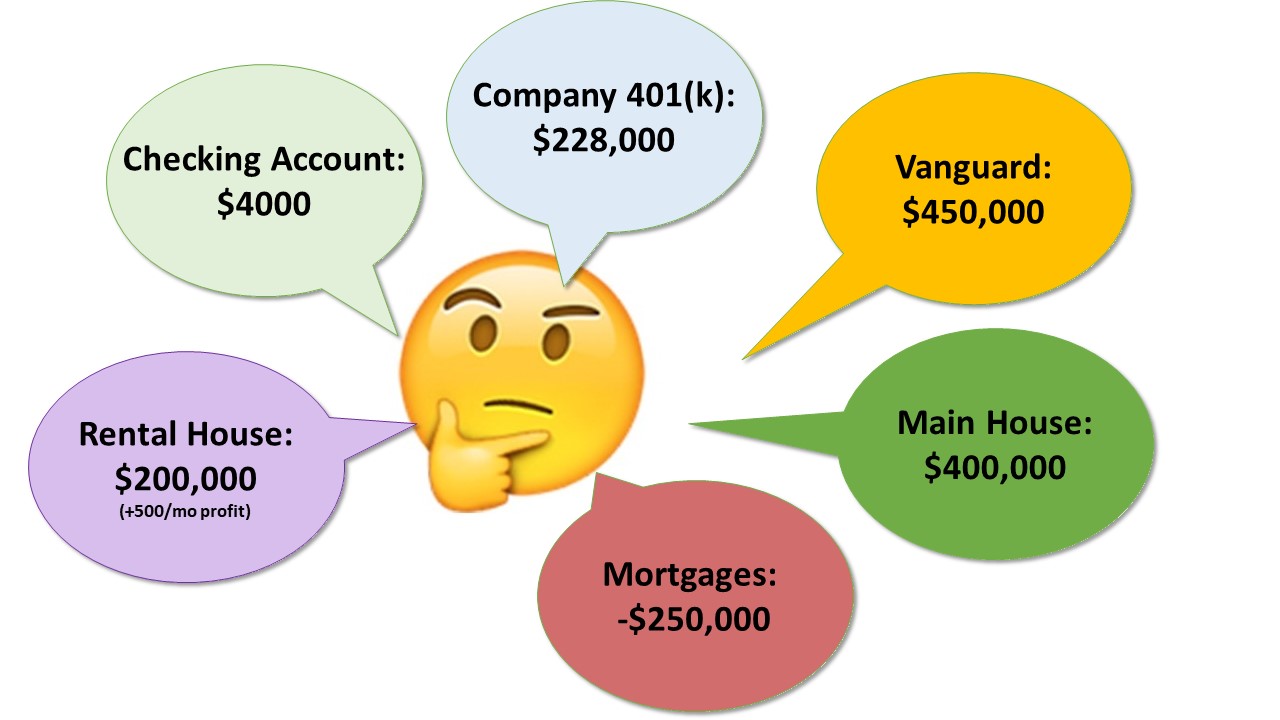

Luc: There are a lot of real estate/rental experts in the Mustachian fold – I am not one of them, but real estate is the main reason we’re now financially independent.

We bought our first house in 1999 with $5000 from my dad and a $3000 courtesy check from Chase. We chose the house because it had a mother-in-law basement, with its own entry and kitchen – we went from paying over $900/mo in rent to having a tenant and paying around $300/mo toward our own house. We were fortunate enough that soon thereafter Longmont housing prices had a nice little bounce.

In 2003 I took out a home equity line of credit and we bought a condo in Fort Collins. A realtor soccer friend had given me a handy little spreadsheet that detailed all the ways to make money from real estate, and at the time it was hard to find cash flow properties in Longmont.

In hindsight, that first condo was a mistake. It was an hour commute to deal with any issues, it wasn’t a place I had much emotional attachment to, and it didn’t attract tenants who cared about it – it was a soulless investment. Nonetheless, we held it for over ten years, and finally saw some significant appreciation in the last few years (and it gave me my first taste of YouTube success with a video on How To Finish a Subfloor.)

I sold the condominium on Craigslist in 2015 and did a 1031 exchange for the Atwood Project – probably the most soulful investment I’ve made.

The lesson I learned from that first condo was that I wanted properties that were in my neighborhood, that I cared about, and that, when fixed up, made our community nicer. And of course they had to make money, too. Again, I was lucky enough that all those things were achievable here in Old Town Longmont, even through the recession.

Over the years, we leveraged our way into four rental properties in Old Town (moving into our current place along the way and turning that original home into a two-unit rental). The cash flow alone allowed me to spend less time painting and more on other pursuits. And my wife was able to move her teaching career down to half-time.

In 2016, I spent an average of under 10 hours per property – over the whole year – on maintenance and administration. Yes, there are occasional shit showers when cleaning out an old lead P trap, but most of it is more pleasant than that.

After finishing up the remodel work on the fourth and final property, we had 100% occupancy in all places and pulled in about $92,000 in rent; $36,000 after expenses.

Meanwhile, our longer term gamble on the livability of Old Town has paid off, as home prices have more than doubled here in the last several years, leaving us with equity close to $1.5 million (including the home we live in). The best example is the Foreclosure Project, which we bought for $113,500 in 2011, put about $25K into it, and is now worth over $300K.

To take some of that appreciation money off of the table, I chose to sell the most expensive of these houses last year, and re-invest the cash into standard stock market investments.

This is where MMM will probably caution you that not all real estate investment will go so well.

Building DIY Electric Cars

Although it’s no Tesla, this little homemade contraption was my first peek at the world of electric cars.

MMM: One of the most technically impressive things to me, was the time you read a book on converting an old gas-powered GEO Metro econobox car into an electric vehicle (EV), using basically a trunkload of golf cart batteries. And then decided to team up with a friend and try the same thing yourselves.

Not being auto mechanics yourselves, what possessed you to do this? And did it turn out to be a good business idea in the end?

Luc: Ha, this was a terrible business idea. I can remember sitting in the office of the City of Longmont fleet manager, trying to convince him to let us convert some of their gas pickups to electric; Fox News was blaring in the background and he was staring daggers at me. Needless to say, we didn’t get that gig, and that was probably a good thing, considering we didn’t have the expertise or capital to pull off truly decent EV conversions.

We did do a couple GEO conversions and an old Ford pickup, which was a lot of fun, but they were novelties more than anything. That was 2009, and it was an exciting time in the electric vehicle world. Lithium batteries were becoming more reliable and less expensive, the movie Who Killed The Electric Car? had come out a few years prior, Tesla was starting to make some waves, and of course addressing climate change was becoming more urgent. I wanted to do something meaningful, and I thought electric cars were the future of transportation. The cash flow I was getting from rentals had given me more free time. And I’m slightly crazy, so why not start an EV business?

At the time, Colorado had an amazing incentive for people to buy EVs. One of my favorite parts was arguing with the clueless administrator of the law for months, and then lobbying for sensible changes and clarification when they wrote the new law.

We spun off a new company, Boulder Hybrid Conversions, with two other guys (with more EV expertise), in which we converted Priuses to plug-in hybrids by upgrading them to a larger battery.

Meanwhile, largely thanks to my partner, our original business morphed from being a handcrafted car conversion hobby, to a reseller of electric car batteries and other components. It became one of the larger businesses of this type in the country, grossing over $1 million a year. I had a lot of other ideas for how we could expand the business, but my partner didn’t see it, so he ended up buying me out for about $125,000 (which, for all the time I put into the biz, turned out to be decent but not extravagant hourly compensation).

Boulder Hybrid Conversions became Boulder Hybrids, specializing in hybrid and EV maintenance and repair. One partner bought the rest of us out, and he continues to grow that business. I now own a 2013 Nissan Leaf and a 2015 Prius wagon (my off-road vehicle) and one share of Tesla, and I look forward to the day when I can buy an autonomous mini-van that will safely transport my family and me to Wisconsin overnight while we sleep.

Dead Pine Trees for Dead Bodies

MMM:

One day, I got an email from you that said, “Well, I’ve done it again – decided to start yet another business. Building coffins from reclaimed beetle-killed pine planks”

So we both reviewed the simple plans from a book you had found in the library, built a prototype of this Dracula-style “toe pincher” coffin, and then you photographed it and put up a website. I gladly worked alongside you because I like hanging out and building things, but I remember thinking, “Luc’s really gone off the deep end here – who is going to buy our DIY coffins??”

What was the motivation and the eventual fate of that coffin venture?

Luc: I started Nature’s Casket in 2009 for the same reasons I started the EV business: to do something meaningful for the environment. And because it was different and exciting. And because I wanted to help my brother with more hours when we had downtime from painting. All the remodel work we had done meant I had most of the woodworking equipment I needed to build coffins. And it was nice to have some technical, logistical, and, hell, labor support from old MMM to get it going.

The green burial movement, already well-established in the U.K., had been growing in the U.S., largely as a result of the Ramsey Creek Preserve, a conservation burial ground that conserves the land in a natural state. Green burial is traditional burial: simple and environmentally friendly (none of the swimming pools full of formaldehyde that are pumped into cadavers, no unsustainably harvested wood, stamped metal caskets, toxic paints, concrete vaults, or pesticides and copious water for manicured cemeteries).

Here in Colorado, the pine beetle epidemic was devastating our lodgepole pine forests, but leaving a lot of dead trees with beautiful blue grain (from a fungus that feeds on the beetle’s waste).

With some support from Karen Van Vuuren, who runs a nonprofit helping families direct their own funerals (and has now started The Natural Funeral), I was able to start getting the word out and selling a few caskets here and there. And it turns out that the media is really interested in things like death and beetlekill wood.

The Denver Post ran a front page article on my business in 2010 – many people saved that article, and when they’re ready, I get a call for a casket (to this day I’m still getting calls from that article). The New York Times mentioned Nature’s Casket (they never contacted me, so my mom was the first one to tell me about that). The Wall Street Journal sent a guy out to do a piece on beetle kill (I wasn’t mentioned in the article, but had a lot of time in the accompanying video). National Geographic sent one of their photographers out to take photos of the caskets at a funeral, but we didn’t make the magazine. There was also a nice story in Longmont’s Times Call newspaper.

Soon I was shipping coffins around the country. One of the most interesting gigs was when we built and reinforced eleven oversized caskets (with MMM on welding and metalworking support) that could hold up to a ton; these were for the reinterment of a 19th Century family cemetery in Virginia that was being moved to make room for a high school football stadium (most of the remains were biodegraded, so they included all the dirt from each plot).

This is where I should mention that I’m kind of success-averse. Nature’s Casket could have been a large business with an industrial shop and a storage warehouse if I had pursued that path. Instead I stopped shipping (too onerous and stressful) and ceased most advertising. Now it’s just a local business, and I average less than one casket a month – it’s still quite rewarding, but there are other projects to focus on.

Miscellaneous Mini Businesses and Pursuits

MMM:

Scattered in among these years were a few smaller things. The time you started designing your own greeting cards and printing them on fancy textured recycled paper. Then there was Simple Brew Kits, which was just assembling the required components for converting good grocery store cider into booze. A photography pursuit that started with just taking your daughter to over twenty of Longmont beautiful parks and ended up culminating in a show at the city’s museum.

Oh! And then of course the time you went to Scotland with two friends and some quickly researched photo equipment and shot a feature length film that ended up in the Front Range Film Festival – despite the fact that none of you had any experience or training in filmmaking. What was that all about?

Luc: Recycled Greeting Cards was actually born in the late ‘90s, around the time I started the painting biz. At one point I had pretty high hopes for RGC, even attending the National Stationery Exhibit in New York. That business was mostly a failure, although I have one loyal business customer who still buys a thousand or so cards a year.

Simple Brew Kits was a business I started for a blog post that I never published titled “How To Start A Business In One Day.” And that’s essentially what I did, filling out all the paperwork and putting up the website in a day. I didn’t sell many, though, until your post about the business, after which I was suddenly inundated with hundreds of orders. That slowly tapered off, and recently I decided to shut it down for good. Again my success aversion won the day. But we made a lot of fun (and some disgusting) drinks out of that whole deal, and I’ll still occasionally bust out some fermented cider or grape juice.

The photography gig was a byproduct of becoming a parent. My daughter was born in the spring of 2006. After my wife’s maternity leave, I became a stay-at-home dad off and on for a couple years. I wanted a project that would get us outside, but that would also provide me with something exciting. I decided we would visit each one of Longmont’s city parks and take pictures. I just had a little point-and-click dealio, but it took decent pictures.

A few years and thousands of pictures later, I chose one photo from each park and submitted the project to the Longmont Museum. To my surprise, they accepted the show, and even helped me publish a book of the photos. It was a gratifying experience and has led to more photography projects – something I’ll continue to pursue.

The Scotland film, Carve The Runes, came from an idea I had many years ago to get a group of friends together, rent a castle in Scotland, and produce a music album (despite having no musical talent). Over time, the idea morphed into making a film instead. I was able to convince my brother Isaac and a good friend, Ian, that this was in fact a realistic and good idea.

And so, in 2015, we spent ten days traveling around Scotland, filming and, well, just filming – we didn’t have time for anything else. I had envisioned some time for fly fishing and golfing in between shoots, but damn, making a movie is hard.

The film is about two brothers, one of whom has a terminal illness and goes to visit his brother in Scotland, where he’s doing climate change-related research. The basic idea for the film was laid out beforehand, but most of the script was written on the fly (I didn’t think we would use a script). Ian was cinematographer/sound guy/key grip/best boy, and maybe more important, moral support. We didn’t sleep much, and we drank a lot of scotch. It took us a couple years, but we finally finished post-production at the beginning of 2018.

We submitted it to a number of film festivals, and were happy to be accepted into our local Front Range Film Festival, where we won Best Feature (out of a limited selection). The acting and cinematography are suspect, but the soundtrack (friends and acquaintances) and screenplay, if I may say so, are legit; I’d love it if we could remake this with some real producers and actors (Francos, Afflecks, are you reading this? Or maybe the leads should be sisters).

A Quixotic Urban Oasis and the Big Dig

A few thousand pounds of concrete? all in a morning’s work.

MMM:

Surely the most concentrated demonstrations of your varied efforts and interests is in your own house. Because we restored it together from its original tippy skeleton into a solid and classy residence. But then a few years later went on to add a two story addition all the way up from the hand-dug structural piers. And then to build the garage workshop which has turned into an enviable hobbit-like enclave of living and productivity, both inside and out.

But all of this pales in comparison to the most recent upgrade, the Big Dig where you hand-dug about 60,000 pounds of concrete and soil out of your own basement (with occasional help from a beer-fueled team of other local Dads) to upgrade it from the typical Victorian house storage cellar into a very functional Man Cave complete with golf simulator and workout room.

What has driven you to go so far, when some people won’t even change a furnace filter? Any downsides and pitfalls?

Luc’s Hobbit-esque backyard oasis and workshop/garage, carved from an area that was originally just weeds and concrete.

Luc: I have labeled myself an eclectic: someone who loves to continually explore new ideas and embark on new adventures. The peril is getting so wrapped up in the novelty component that one never finishes anything – what I call dilettantism. This is part of my success aversion: I love to get a project or a business up and running, but it’s hard to continue to find it rewarding once it becomes quotidian. Routine is anathema to eclectics. Most of my projects reach a level of fruition that’s satisfactory to me, but I still think I can strike a balance that leaves things more complete.

To use my house as a metaphor, I’ve completed a number of satisfying projects (with a lot of help from people like you (mostly you, in fact)), but in the meantime many of the details have been overlooked: we need a new kitchen faucet, a toilet needs to be re-seated, I could organize the cookware situation better (and oh, by the way, I should probably spend a little more time with the family).

In the mid-aughts, I was working on figuring out what I wanted to be when I grew up – I decided to embrace my eclectic nature. Now in the late teens, I’m realizing I need to fine tune that to incorporate more focus, responsibility, meticulousness and perseverance.

Physical Fitness and Doing Experiments On Yourself

MMM: Another unusual trait I’ve noticed is that you seem to operate in extremes. You can eat a plate of cookies or drink a bottle of wine in one sitting, but then also go for three days straight with zero food during a fast. You’ve tried a variety of 30-day experiments in different eating styles, following them up with weigh-ins and blood tests to see how they affect your good and bad cholesterol counts. You adopted weight training and have stuck with it for many years now.

This is different from my own approach, where I eat roughly the same thing year after year, making only small tweaks – like I lift heavier barbells and eat more carbs if I want to gain weight, and cut out beer and go to bed hungry when I need to lose fat.

Have you noticed anything about the Human body and what makes it function best? Any advice for people who are prone to binging, on getting control of their eating and drinking habits?

Luc: Oscar Wilde, perhaps after bingeing on absinthe, said “Everything in moderation, including moderation.” That was kind of my motto for much of my youth, and it fits well with the eclectic personality. But if you only practice moderation in moderation, I discovered, you tend to feel like shit a lot and you weigh about 20 pounds more than you should. I’ve modified the motto to Everything in moderation, including gluttony.

I think everybody’s different in terms of what works best for them to stay in shape and feel healthy, but there are some common threads. In our simple carb-y society, one of the easiest ways to eat better is to cut out most simple carbs (but, if you’re like me, allow yourself an occasional plate of cookies).

After all my fasting and intermittent fasting and super low fat and super low carb and alcohol temperance experimenting (and reading the research), I’ve come to a few fairly simple conclusions. First, a low glycemic diet (like the Mediterranean diet) seems to be the best. And eating within a fairly small window each day, say from noon to 6, is healthy. Of course, less alcohol on a daily basis is good.

With the new gym, I plan to have a regular but varied workout that includes weightlifting and short bursts of intense cardio on the bike. And, for eclectics like me, mixing it up and allowing myself to occasionally break the rules is key to continued success.

The YouTube Channel and Online Pursuits

At some point, I remember you started documenting your projects on YouTube. This has grown into a bit of a “channel” where at least one of your videos has over 100,000 views.

I have always hesitated to put up videos myself, because so much of YouTube is slickly produced and well-edited today and I am shy to put up my amateur work – much like the fearful theme that started us off on this whole article today. But you didn’t seem to care, and you just did it, and now the channel is out there.

How has your YouTubing experience been and do you have advice for anyone else? How hard would it be for a YT channel to become a successful business?

Luc: Ha ha, yes, the YouTube project has been quite an adventure. Currently there are three videos with over 100,000 views, including the Atwood remodel video, with over 750,000 views (you’re in that video – how does it feel to be a rock star?). What’s funny is the Atwood video was really poorly produced, yet it still somehow went semi-viral in the spring of 2017, spiking from an average of about 400 views a day to a peak of 21,000 views. That tapered off over the next year and a half, but I’ve made almost $1500 on that video. I’ve been trying to push the traffic from that vid to an updated and better produced version of the video, with limited success.

Like a lot of my other projects, the YouTube project has been a gung ho endeavor, jumping in with both feet in spite of limited skill and experience. A more well-thought out plan, executed with better focus, may have lead to more success. Then again, it might not have gotten off the ground if I had been too cautious.

In my newly grown up and focused life-phase, I hope to grow the channel into one that attracts more subscribers and maybe even provides enough income to buy more than a meal out on the town every month. Still, I have to keep that eclectic feel – I mean who doesn’t want to see everything from remodel work to creative pumpkin carving to insect eating to casket building to Trump parody to crazy body hair shaving? I have about 30 projects in the can as we speak, just waiting to be edited and uploaded.

(MMM note: did you catch that? Thirty projects we haven’t even mentioned in this article, including the time he tried to earn a Guinness world record by carving a 27 foot “Mustache” into his own body hair?)

The best advice I can give to aspiring YouTubers is don’t have a shaky camera – man does that drive people nuts, as I’ve been told again and again by people who watch the original Atwood video (there’s a lot of anger out there, as you well know, MMM). There’s something to be said for the amateur folksiness of YouTube, but there’s a balance between unwatchability and being too slickly produced (I’m still working on finding it). I’m probably the wrong guy to ask about what people want to see, but I imagine it’s pretty much anything you have an interest in, as long as the video is useful or entertaining.

Financial Independence and What’s Next?

Neighbourhood friends sampling Luc’s Sauteed Crickets at a party

MMM: As the years have gone on, you’ve remained a self-employed person and never stopped working hard on things. But I have noticed your work progressing from hardcore grinding out of professional painting jobs near the beginning, to more eclectic stuff now that is less income oriented. For example, the time you raised edible insects in your basement and researched and wrote an academic paper on how good it would be for the world if we switched some of the rich world’s meat consumption over to nutritionally superior stuff like cricket flour or bee brood. Not a lot of money in that type of thing, at least not to pay this month’s grocery bills.

What has been your secret to this decreased pressure on income making, and would you say you have a better work-life balance now than you had back in 2005?

Luc: Primarily because of my real estate investments, I’m fortunate enough to be in a position where most of my projects don’t need to make money. To me, the end goal in life is fulfillment, and the only way to achieve fulfillment is by making the world a better place, whether through service to the community, producing beautiful works of art, fighting for peace and justice in the world, writing a blog that denounces materialism and promotes sustainable living (wink wink), or just by being a good person to those around you.

A lot of my projects still focus on things that improve my own life, but more and more I hope to work on projects that help others, from the hyperlocal (being a better father and husband and friend) to the local (being more involved in our community) to the global. On the local front, one project you and I have worked on a little together is trying to get more solar power in Longmont. On the global level, I’ve been working with my father, E.G., on The Cooperative Society Project, a decades-long project that looks at the potential for humans to make the transition to a new stage of human interaction: one driven by cooperation rather than conflict.

The way I see it, the beauty of financial independence isn’t freedom from work, it’s the freedom to work on a fulfilling life.

An Afterword from MMM:

So this is a long article. What does it have to do with YOU and your own financial independence?

I have wanted to share these tales because they’re a great example of the idea of living with less fear. The neat thing about Luc’s entrepreneurial ventures is that he is willing to do things, even if he’s not skilled or experienced at them. They often don’t pan out, and that’s okay, because it’s okay to fail. In most cases, failure is just a lesson that leaves you further ahead than when you started, with some great stories to show for it too.

But to minimize the damage of failure and maximize the chance of success in entrepreneurship, Luc and I have both noticed a pattern over these thirteen years:

-

Start Small and Just Sell Something – most failed businesses start with borrowing and risk. Instead, you should find a customer first and get them interested in buying your stuff. Only after the sales come, should you reinvest some of this money into a bigger business.

-

Hard Work Can Save You from your Mistakes – when you’re getting started in anything, you will make expensive mistakes. But you can dig in harder and correct them and learn from them. You need to be willing to launch the business out of your spare room, be your own janitor, and make late night runs to the supply store or the post office to get those shipments out. Plenty of time for kicking back and gathering passive income later on, once the business is profitable

-

Keep Life Simple, Frugal and Stay Focused – a business takes time to build and it takes a while for it to start producing money. But if you enjoy it as your source of entertainment, it will naturally get the time it needs: Spend your weekends in the workshop instead of the golf course or the ski hill. And if you let go of material desires, you won’t be nearly as hungry for money. So while a $20,000 per year hobby business won’t even cover the lease payments on your neighbour’s pickup trucks, it may be more than enough to keep you well fed and happy, for life.

If you’ve got a lifestyle business that you love, feel free to share it in the comments below and inspire the other people reading alongside you.

—

* In this article I profile Luc, but he is of course part of a hardworking and resilient family of four. His wife is also a friend of mine and an equally wonderful person, but I have kept this story just focused on Luc in the interest of the privacy of the rest of the family.

Further Reading:

Poppa’s Cottage YouTube Channel

Poppa’s Cottage Blog

Updated Atwood Remodel Video

Carve The Runes Trailer

How To Build A Coffin Video

Portraits of Longmont Parks

The Potential For Entomophagy To Address Undernutrition