It’s May, which means college graduations are taking place across the country. The transition out of college and into your first job can be challenging, as new opportunities and new responsibilities are quickly put in front of you.

That’s why I thought it would be a great time to put together advice from myself and my amazing network of personal finance peers for all the new graduates out there ready to strike out on their own.

We’ll break out the pointers into three major sections - Employment/Income, Savings/Investments, and Budgeting/Spending.

I really encourage you to read all three sections. Personal finance is holistic; mastering any one of these while ignoring the others is going to give you much poorer results than doing your best at all three.

Fair warning, though - there’s a lot of information below! It may be a good idea to tackle one section of the post at a time :)

Employment & Income

There are lots of resources out there on how to make great resumes and cover letters and how to nail that interview, so we won’t cover those here today. Let’s fast forward a bit and say you’re in the wonderful position of having one or more offers in front of you and you’re trying to figure out which job to take.

Pick the Right Job

If you’ve got multiple offers, don’t just make your decision based on the salary. Here’s why:

- If the jobs aren’t located in the same city, it’s not an apples-to-apples comparison because the cost of living in each city could be different. I remember when I was graduating from college, I had an offer in Chicago that was 10% higher than my job offer in Madison. After taking the cost of living into account, the two ended up being roughly the same in terms of how much I’d have left after expenses.

- Salary is just one piece of the puzzle. You should also compare benefits; if Job A has a killer healthcare plan, that might save you thousands of dollars a year. If Job B has a better retirement plan, that could tip the scales.

- Beyond the financials, look at the “squishy stuff.” Which job has a better path for advancement? Which job has a team and leadership that you can learn from? Which job will better train you in skills that are transferable should you choose to change jobs later on?

- Finally, remember that your first job likely won’t be your last. If you take a job and it’s not a good fit, that’s ok. You have the chance (and the right) to try something different.

Negotiate Your Starting Salary

In the process of picking your job, I’ll also encourage this: negotiate your starting salary. I know that can be intimidating, but raising your starting salary can have a big impact on your long-term earnings.

If you have other job offers with higher numbers, use those as leverage. The conversation could go like this:

Working here would be my number one preference. I think this place is a great fit for me and I know I’ll bring a lot to the position to help you be successful. That said, I do have some competing offers with higher salaries. Is there room for negotiation in the salary you’ve offered me?

Phrased this way, you’re not saying that you’d turn down the existing salary, but you are advocating for yourself to get something better. It doesn’t hurt to ask - the worst they can say is no. If that’s what happens, then you can choose whether or not the original salary is good enough.

Always Do Your Best

Once you’ve got that job, work hard and do your best. When getting your first job, the things that determine your salary are your degree, your GPA, and what potential the hiring manager sees in you.

After that, you’ll find out that those things very quickly lose their importance. Your raises, promotions, and anything else all come down to one simple factor - what value you provide to the company.

There will always be someone who has a better name, better connections or more God-given talent; the only thing you can do about it is outwork them.

Michael Dinich, Your Money Geek

But Don’t Burn Yourself Out

Let’s not misconstrue that last one as a suggestion that you should work 90-hour weeks though. Burnout is real - I’ve experienced it firsthand - and it can be detrimental to your health and your career.

Here’s something important to remember: good companies don’t measure their employees by their inputs (like how many hours you work); they measure employees by their outputs.

Find ways to optimize everything you work on. Look for things that you have to do over and over again and find ways to automate or simplify them. If you can get done in 35 hours what someone else does in 50, you’ll be able to work a 40-hour week and still provide more value to your employer.

Read Your Benefits Handbook

Employee benefits make up about 30% of your paycheck. But if you don’t know what they are, you can’t be sure you’re getting all 30%.

Most benefits handbooks are written in overly-formal language, often bordering on legalese. But it’s in your best interests to hunker down and read each section so you can understand all of the benefits your employer offers you.

So, read your handbook. Then read it again. For areas you don’t understand, ask your human resources department or your manager. Ask friends or family members who have been in the workforce a while what everything means and see what makes sense for you.

Savings & Investments

OK, now that you’ve got that job picked out and know what to do once you get there, what should you do with those paychecks as they start coming in?

Everything in this section will center around a fundamental principle of personal finance:

Pay Yourself First

What does that mean? It means that you should be setting money aside for your longer-term goals before looking at your expenses. The easiest way to do this is to start with your very first paycheck; once you get accustomed to spending a certain amount of money, it’s a lot harder to scale back.

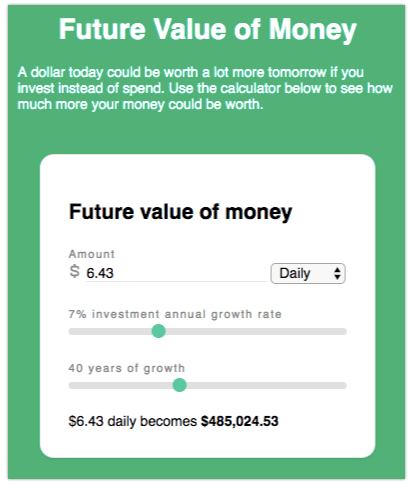

Saving and investing early in your career can drastically improve your finances when you’re looking to retire (and earlier). Investing $5000 a year starting at age 27 (with a 7% return rate) could lead to a $1 million nest egg at retirement. Starting just five years earlier at age 22 bumps that number to over $1.4 million!

Further Reading:

Convinced? Ok, let’s take a look at the ways to pay yourself first.

Understand Your Retirement Benefits and Take Advantage

Does your employer offer a 401k retirement account program? If so, there’s a good shot that they also provide incentives for you to contribute.

Many employers will match the money that you contribute to your 401k either on a dollar-for-dollar basis or a 50% basis. This is free money, but you only get it if you invest in your 401k.

Let’s take an example. Say you make $30,000 a year and your employer offers to match 50% of the contributions you make (up to a maximum contribution on your end of 8%).

- If you put in 4% ($1,200), your employer will kick in another $600.

- If you put in 8% ($2,400), your employer will kick in another $1,200.

- If you put in 12% ($3,600), your employer will kick in that same $1,200 because you’ve exceeded the matching limit.

The key here is to think of that money as a bonus, but that bonus is only contingent on you doing something that we’ve already established is good for you - paying yourself first.

In the example above, if you simply pay yourself first with at least 8% of your salary, you get the equivalent of a 4% annual bonus from your employer!

Sunburnt Saver agrees that starting early and saving through a tax-advantaged retirement plan is best: “You’re already used to living on little and honestly won’t notice 10% being invested for you. It reduces your tax burden (this will matter, I promise) and will help you get a big head start on saving for retirement.”

Pick Your Investments Wisely

You don’t have to be a finance guru to invest wisely. In fact, the biggest finance guru out there (Warren Buffett) says the simplest strategy is the best - investing in index funds.

An index fund is an investment that tracks what the stock market (or another asset class) does in general. Over the long haul, the stock market has a great track record of going up. At the time I wrote this, there hasn’t been a single 20-year period of the S&P 500 (which has been around since 1871) where the stock market lost money.

Given that you’re just getting out of school and normal retirement is ~40 years away, you’re probably good to get started.

Note: there are no guarantees in the market; past performance is not a predictor of future performance. For past performance numbers from above, see this awesome calculator from DQYDJ

The reason Index Funds are so popular with Warren Buffet and others (like me) is because they have very low fees. Whenever you buy a fund, you’re paying someone to manage that money, but index funds tend to be significantly cheaper than others. Whenever you’re dealing with compounding interest, small amounts can be amplified into big ones, so minimizing your fees is critical.

Further Reading:

Pay Off Your Debt (ASAP)

If you’ve got student loans, credit card debt, or car loans, it’s time to start paying them down aggressively. Minimum payments may get you debt-free eventually (if you don’t accrue new debt), but the amount of money you waste in interest could cripple your finances.

There’s no bad way to prepay debt - just a good way and a better way. Find any extra money you can and apply it to either your highest interest loan (the better way) or the lowest balance loan (still a good way) that you have.

To learn more about these methods of paying down your debt and how much money you can save, check out my post on Debt Snowball vs Debt Avalanche.

One of the magical things you’ll find about paying off debt is the amount of freedom in your finances once the debt is gone. If you’ve been paying 50% of your income toward debt, you’ll feel like you got a 100% raise once you’re done paying it off!

Further Reading:

Automate Your Savings & Investments

Set up direct deposit of your paychecks with your bank. And if your employer’s payroll system allows it, split each paycheck into different buckets. Consider funneling a portion off to a “debt payoff” savings account so you’re not tempted to spend it.

You can do the same for establishing an emergency fund. If you put aside just $8 a week for an emergency fund, you’ll have $400 saved up after a year, which puts you better off than the 46% of Americans that can’t handle an unexpected $400 expense.

We set up a savings account for everything - emergency savings, travel, home remodeling, kids savings, the list goes on. We do our banking with Capital One 360 because they have reasonable interest rates and make it ridiculously easy to set up new savings accounts. At one point, I had my paycheck getting split into 5 different accounts to “pay myself first” and work toward my financial goals.

Seller At Heart recommends putting $100 from each paycheck into a side savings account that you don’t have a debit card for. That way if you need the money, you’ll have to go to the bank and wait 2+ days to get the funds transferred. The inconvenience will prevent you from spending it unnecessarily.

Budgeting & Spending

If you’re still with me at this point, I know you’re going to be successful - it takes a lot of patience to dive this deep into a money article!

Let’s talk about budgeting and spending, but we’ll start with a couple questions.

Did you live like a king or queen in college?

Probably not.

Did you still have fun?

Probably so.

This is an important lesson to remember. Your income and living situation in college probably wasn’t luxurious, but you still found happiness and joy.

As you transition out of school and into the working world, there will be a lot of temptation to succumb to “lifestyle inflation.”

Avoid Lifestyle Inflation

Lifestyle inflation is when you find yourself spending more because you make more. If you can avoid that trap, your raises and promotions can help further your long-term financial goals instead of just getting you an extra scoop of ice cream whenever you go out.

Your spending and income should only be loosely related - in that your spending should be less than your income. When your income goes up, it’s a great opportunity to pretend like that never happened and instead funnel more into savings and investments.

Some amount of increase is realistic; after all, your life is going to change. Someday you may have kids, buy a house, or travel more. You might want to sleep on something other than a futon. But remembering that you can live on less and still enjoy yourself is a powerful, freeing mindset.

Save it Before You Spend It

One of the big consumer traps that trips a lot of people up is getting in the habit of buying things on credit (either through a credit card or through a loan - AKA financing). Even when the purchase is at 0% interest, this is dangerous. Here’s why:

It’s a reversal of the money timeline. Buying something on a credit card today and then paying it off at the end of the month can lead you to spend money before you’ve earned and saved it.

Life is dynamic and you don’t know what the future will hold, so the safest course of action is to live by a simple rule:

Save it before you spend it (Tweet this )

If you follow that one little rule for everything in your life (except maybe getting a mortgage for a home), you’ll have a whole lot more security!

Make a Budget

If you know what your income is and you know what you want to set aside to pay yourself first, then you’ve got the remaining amount for your budget.

Creating your first budget can be hard. After all, how do you know how much you’ll be spending on stuff?

The answer is that you probably won’t.

Your first budget will be imperfect. You’ll overestimate some expenses and likely underestimate many more. You’ll forget about the random things (like annual car insurance) and be taken off-guard by the unexpected (like being asked to be a part of someone’s wedding and having to pay for a dress or tuxedo).

But the best thing you can do is to create a crappy budget and then improve it from there.

Every month, you’ll better learn your spending needs and habits and will be able to refine your estimates. After a full year, you should have a good sense of where you’re at and your confidence will grow after that.

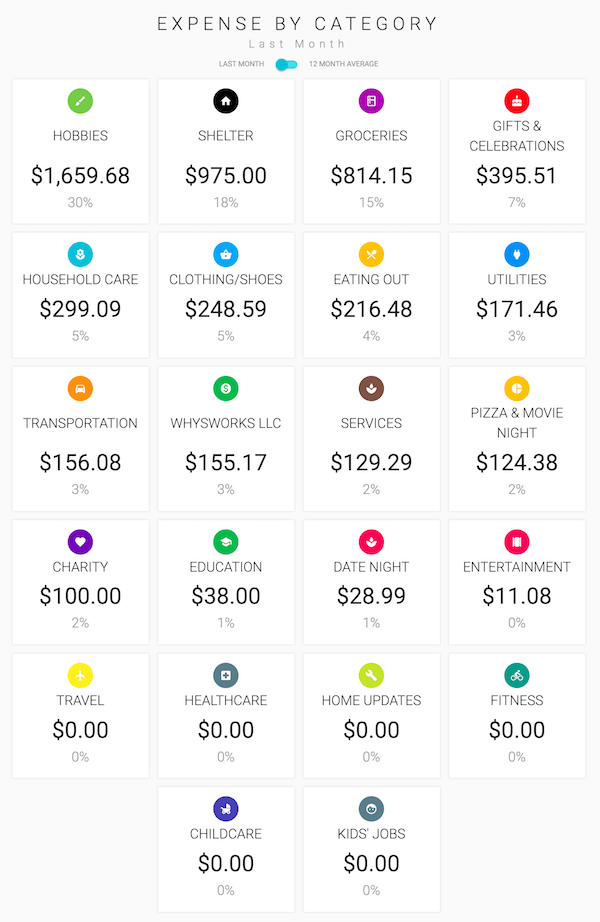

When creating your budget, it’s helpful to break things down into categories. Here are the ones I recommend starting with:

- Charity

- Clothing/Shoes

- Eating out

- Education

- Entertainment

- Fitness

- Gifts

- Groceries

- Healthcare

- Hobbies

- Household care (cleaning products, etc.)

- Pets

- Services (haircuts, life insurance, etc.)

- Shelter (rent/mortgage, renters/homeowners insurance, etc.)

- Transportation (car, gas, auto insurance, public transportation, etc.)

- Travel

- Utilities

Track Your Spending

A budget is great, but if you don’t track your spending, you won’t have any accountability.

There are tons of ways to track your spending, and you just have to pick what’s right for you:

- Track on paper or in a spreadsheet on your computer

-

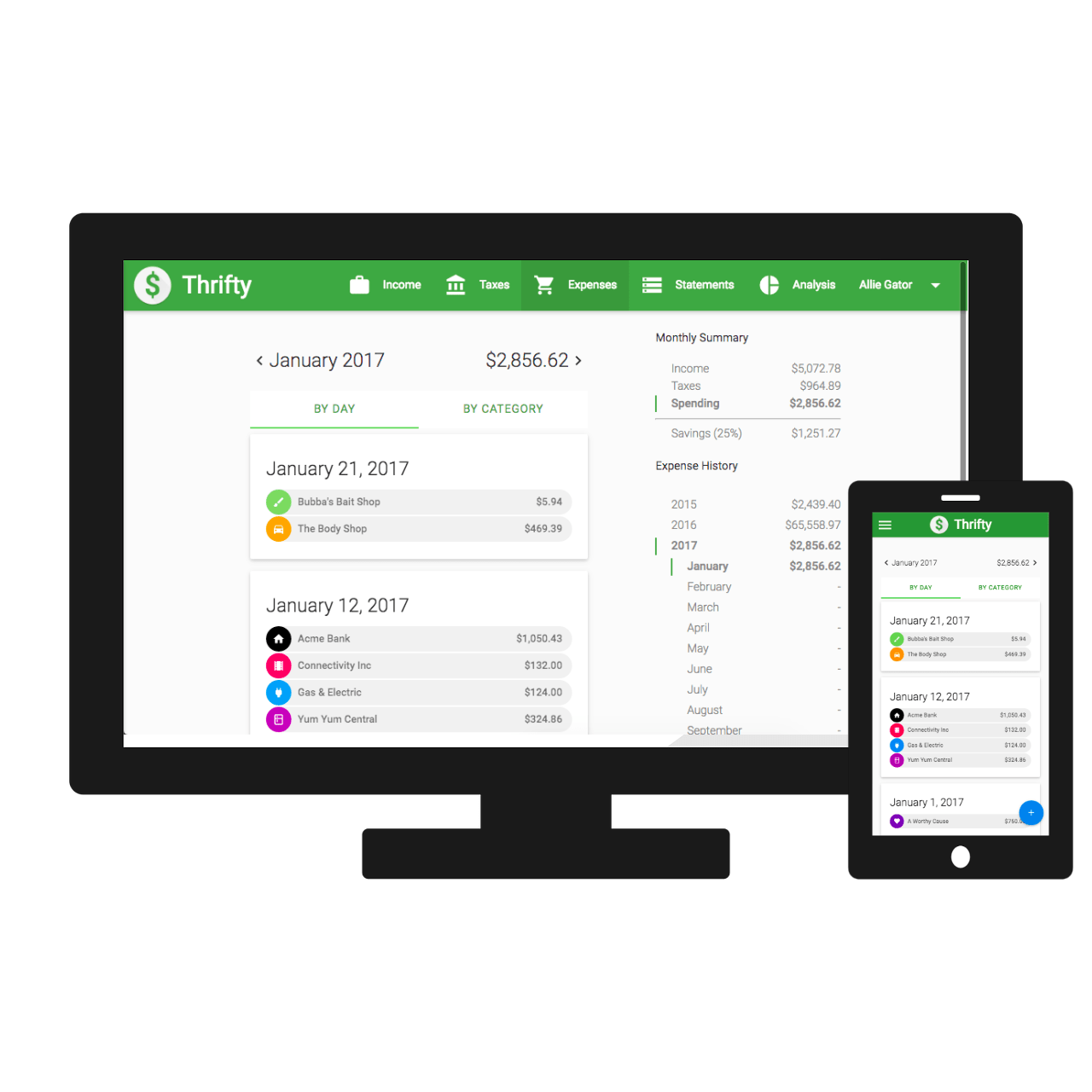

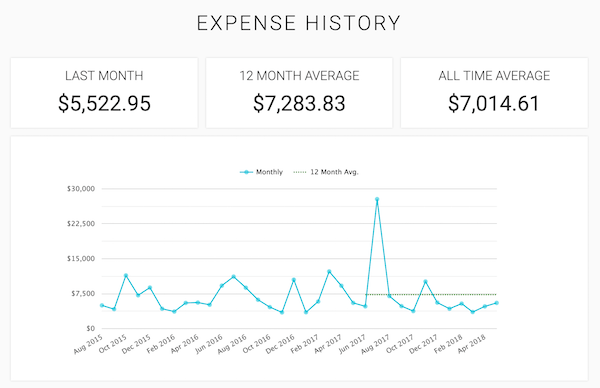

Use Thrifty, the money tracking app we made. It comes pre-loaded with all the budget categories I listed above and you can create your own as well.

- Use Personal Capital, an automated expense and investment tool

As you track, you’ll find out what your spending habits are - both the good and the bad. Look at the categories that take up the most of your spending and see how you can improve. Most likely the big three are going to be shelter, transportation, and food.

Let’s take a look at how you can save on each.

Saving on Shelter/Housing

Remember what I said earlier about living on the cheap in college but still having a good time? Yeah, the whole thing about lifestyle inflation.

Chances are, you spent at least part of your college career with roommates. It’s tempting when you graduate to feel like you “deserve” to live on your own, but that is going to come with a hefty price tag.

When I graduated college, a one-bedroom apartment would have cost me $750 a month in the Madison area. Instead, I got three roommates and we rented a 2500-square-foot house with 4 bedrooms and 4 bathrooms, paying just $375 a month each.

That’s a savings of $4500 a year!

In addition, those roommates and I split utilities and had a built-in support network if we needed any help from each other.

Further Reading:

Saving on Food

Personal Finance for Beginners nailed this one:

When you start working a 9-5, it’s tempting to go out for lunch with coworkers every day or grab dinner on your way home from the office. Without a budget, it’s easy for your food spending to spiral out of control. It’s important to create a budget/goal for food spending and learn a few basic tips, like buying in bulk, learning how to cook, and setting aside time each week to meal prep!

If you’re looking for ideas, PF Geeks has a list of 46 recipes that you can make for less than $2 a serving.

Saving on Transportation

Do you already have a car? Great! That means you don’t need to lease or buy a new one.

You may even explore whether you need a car. Are you in a place with good public transportation? The license, insurance, and maintenance of a vehicle may be an unnecessary expense.

If you do need a car and don’t currently have one, don’t be tempted to use your newfound purchasing power to get an extravagant ride. Cars, by-and-large, provide the same function whether they cost $3,000 or $300,000.

If you need a car to get to and from work, to visit family, to run errands, and go out with friends, buy something that will perform the function of doing those things. Anything beyond that is a status symbol, and those status symbols can drain your bank accounts.

As Winning Personal Finance points out, your car could be costing you millions

Further Reading - Other Personal Finance Tips for New Graduates

If you’re looking for more ideas, check out these other great resources to help you get started with money after graduation:

Parting Thoughts

Phew - That was a ton of information! There’s a lot to take on here, so I’d like to leave you with a few parting thoughts.

Understanding everything you need to know about money as a new grad is no easy task. Turning those into practice is even harder. You’re going to have slip-ups and mistakes and that’s ok.

You won’t be perfect with your finances, and that’s OK

Try to do something every week to improve your financial situation. Learn from your mistakes and keep an eye on the goal.

Oh yeah, that reminds me of an important one. What is the goal anyway?

Don’t make the mistake of thinking money is the goal. Money is a tool to help you achieve the goal. (Tweet this )

Money is necessary and it’s a powerful tool to open up doors in your life. But it’s not the end-game. It won’t give you everything you want and you won’t get to take it with you when you die.

Use your money to help you live a fulfilled life, focused on your relationships, your passions, and serving a higher purpose.

Don’t be afraid to ask for help

Money is complex and there’s a lot to learn. So don’t be afraid to ask for help. We’ve all been there. I didn’t understand compound interest until my dad explained it to me. I didn’t know the difference between a 401k and an IRA until I dove into the details and picked my coworkers’ brains.

If you have questions or need help, find me on twitter or leave a comment below. I’ll do my best to give you an answer or find someone who can.

Congrats on your graduation and best of luck in this next big phase of your life!

What advice do you have for new graduates that you wish you had known? If you’re a new grad, what money questions are keeping you up at night that we can help with?